Professor Robert J Shiller won the Nobel prize this year (with Eugene Fama and Lars Peter Hansen) for his work on the analysis of prices of various assets. He repeated his Nobel lecture at the Yale School of Management today, and I grabbed a couple of screenshots from the livecast.

His early work tested whether the value of shares is equal to their future dividend streams, and it did. Later he observed that the volatility of share prices (against his model) was mainly due to “innovation” from the companies and the market.

Picking Stocks

For me this means investors should hold stocks in companies which have secure dividend streams for regular portfolio growth (e.g. Meridian), pick stocks in companies that will deliver disruptive innovation to get outsize returns (e.g. Xero), and avoid stocks where the companies are subject to being disrupted by innovators and are unable to respond (e.g. Yellow).

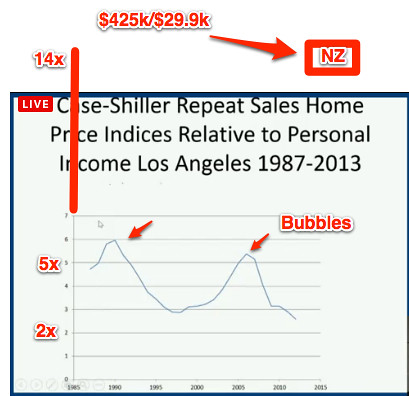

Later in his career Shiller came up with the definitive house price index for the USA, which tracks prices for repeat sales:

I raise this because he then put up a slide of Los Angeles house prices versus personal income, relating a story about how extreme ratios a few years ago made it hard for people to choose move there.

So how are we doing in New Zealand? Even I, a housing price cynic, was shocked by the result when I crudely replicated the analysis.

Our latest median house price, states REINZ, was $425,000 in November last year. The latest statistic for median income in New Zealand from NZ Statistics is $29,900, from the June Quarter last year. That gives a ratio of $425,000/ $29,900 = 14.21.

That wouldn’t even fit on the chart above, so here’s how it would need to be amended to show New Zealand.

A bit more searching and I found the 2004 paper where Case and Shiller asked “Is there are bubble in the housing market?“, and showed that while for most US States the housing prices were directly related to income, but a few (about eight) states were well out of whack, showing more volatility along with higher average ratios.

Picking Bubbles

The chart that Shiller showed above shows that the LA prices dropped by over 50% versus income from 2006 until now. My own take is that there is clearly also room in New Zealand for a very very steep plunge in house prices. It would need a catalyst, but let’s remember to not blame whatever that catalyst is, but the system of incentives that has delivered us this ridiculous and very dangerous situation.

And remember – if you are selling your house, then its smart to do so using the latest tools, real estate agent experience and low commissions at 200Square.

Update:

I forgot to add into housing index that Shiller put together. How I would love to invest (short) on this for NZ.

Hey,

Interesting stuff for sure, in line with the Economist index:

http://www.economist.com/blogs/dailychart/2011/11/global-house-prices

When people in NZ are talking about a ‘supply issue’ they are not just talking about zoning and density restrictions, but also the replacement cost of property (which is pretty high in NZ at the moment). However given that, and given rental returns, there is definitely a sizable risk of a downside correction in house prices.

In terms of the broader economy, the banks are reportedly holding sufficient capital to deal with a sizable correction – so a correction shouldn’t lead to a financial crisis, and shouldn’t necessarily lead to a large recession. However, shocks don’t come all at once – the risk is that the correction in house prices occurs because of some external shock (eg a slowdown in China, and corresponding collapse in commodity prices). That type of shock, combined with a correction in house prices, is the type of risk that has the RBNZ and many analysts so uncomfortable in the current environment.

LikeLike

You’ve seen Hugh Paveltich’s stuff at Demographia, no? Here’s their 2013 survey.

Click to access dhi.pdf

They use median house price to median household income as their standard measure. We’re out of whack high here, but not as bad as the numbers you’ve got up. And it’s been that way for a while – I’m not sure bubbles can last for a decade.

I’ve tended to argue that we consequently need the following mix:

1) Have the majority of city areas come under the least restrictive density rules to allow developers to increase density where it makes sense to increase density [you might need to add in set fees that compensate neighbouring properties to avoid some of the NIMBY opposition];

2) Make it easier to run greenfield development on the edges of town through use of Municipal Utility Districts instead of development charges. Councils seem to like putting in development charges that are high enough to extract rents from developers rather than cover the costs of development. MUDs let the buyers of new greenfield suburbs cover the infrastructure costs themselves;

3) Put in congestion charging (time-of-day and route-specific road user charges) to deal with the most substantial negative externalities of both of these.

Crazy high property prices because of zoning restrictions mess everything up. Too much wealth gets tied up in housing and cities become ridiculously fragile to natural disasters (look at how nothing got done for three years post quake in Chch on housing).

LikeLike

I had not seen it – thanks.

Demographia’s data had Auckland median house price at $506,000 – latest is $620,000.

Demographia’s data had Auckland household income at $75,000 – latest is $76,024

So Auckland’s ratio, already in the worst bucket, has gone from 6.7 to 8.1.

Only 7 out of the 337 regions sampled by Demographia had a ratio higher than that.

LikeLike

Oh. Yikes.

We need to find ways to make it be in Councils’ interests not to let this kind of thing happen.

Existing homeowners love runups in house prices and love complaining about any neighbour’s attempt at subdividing or putting up townhouses. Councils seem pretty sensitive to those concerns and don’t seem to give much of a whit about the broader effects. And so we get strangleholds: the anti-sprawl people block anything on the edges of town; the NIMBYs block anything in-town. Cities can’t go up or out so prices go up instead.

Not sure what the best answer is. But shouting about it hasn’t done much good as yet. I think we need to find ways of changing Councils’ incentives such that they want the change to happen too.

It amazed/freaking annoyed me that it took three years after the earthquake here to even get Christchurch Council to agree that it should be legal for somebody to build a secondary flat with a kitchen in his house. The single simplest way of getting more housing post-quake, and Council planners flat out refused to let it happen.

LikeLike

Hi Lance,

What is your thought on the view of Positive Money – http://www.positivemoney.org.nz. I tend to see that banks being able to creat virtual money is a large part of the problem. Another solution I fell is going to be the introduction of a proper pre purchase report. In the UK for example the vast majority of people will instruct a Chartered Building Surveyor to undertake an inspection. They will pick out maintenance and defects to a much greater detail than a builder. If most houses in NZ were scrutinised by a CBS and had to actually have a warrant of fitness that included energy efficiency and durability we would easily stop the over inflation of property prices.

LikeLike

It would be an interesting experiment for lots of existing home owners to calculate what their current ratio is to see where they fit on the scale. Also would be interesting to then figure out which area they *should* be living in, in order to get on the “Affordable” section of the scale. e.g. a couple with a combined income of $150k would need to buy a house for around $450k to be classified as affordable, and Trade Me currently lists just 20 houses with 3 or more bedrooms in Auckland between $400k and $450k.

LikeLike