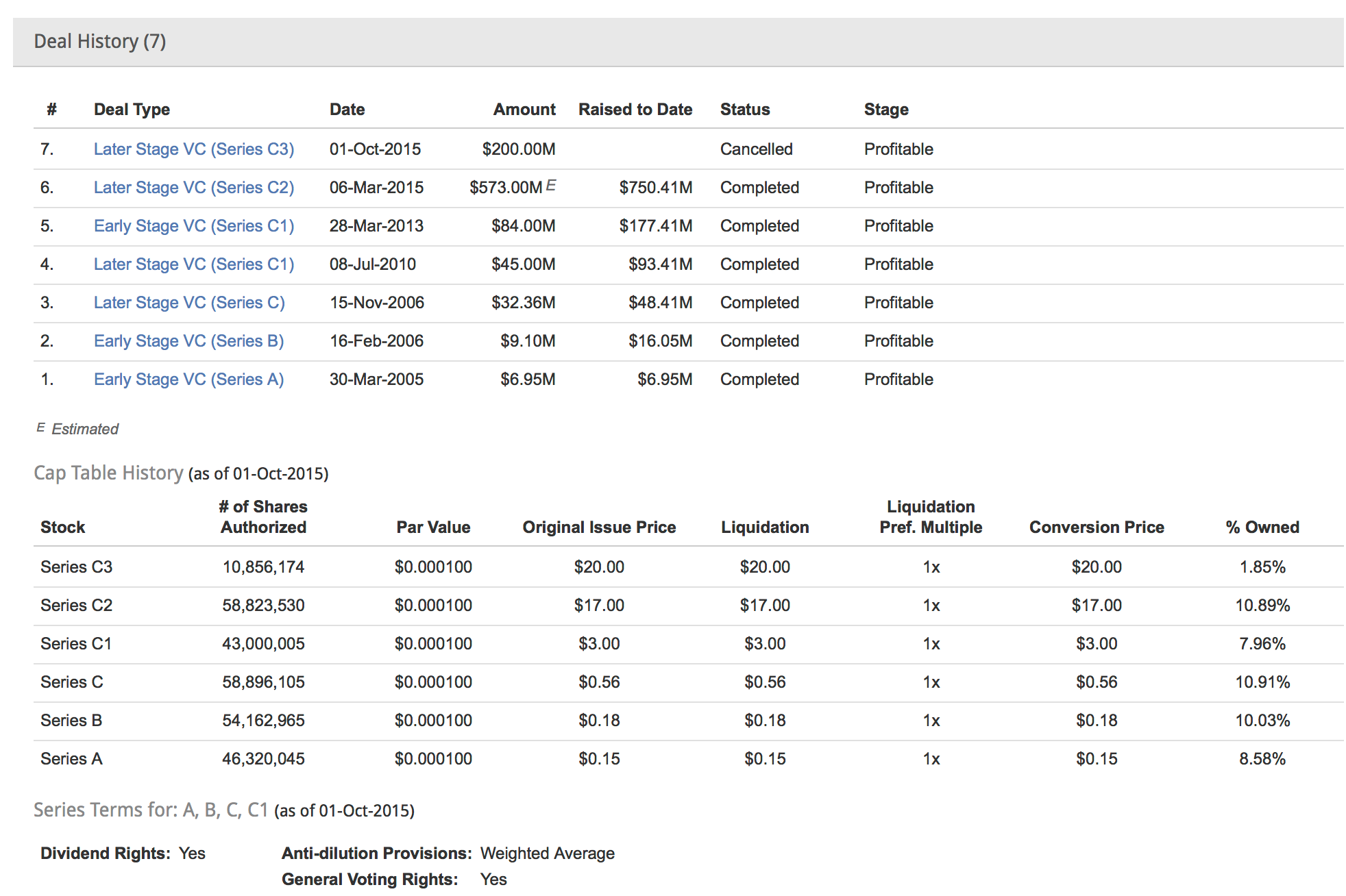

The last round of VC investors into Theranos makes for somber reading. In March 2015 Theranos raised an estimated US$573 million for their 6th round, making a total of $750 million raised. Their 7th round, for $200m, has apparently blown up before completion. Theranos was selling a blood testing service that apparently needed tiny amounts of blood to work.

The 5 investors from March 2015 should be deeply ashamed, as should those who almost committed in the 7th round.

(Source: Pitchbook)

The Wall St Journal broke the story first, and a few weeks later it seems clear that their blood-testing technology is hokum, their partnership with huge pharmacy chain Walgreens now dissolved and the company under criminal investigation. The reputation of once superstar CEO Elizabeth Holmes is in tatters.

It’s every investor’s nightmare.

So how do you stop this sort of dumb investment happening?

At the earliest, and every, stage in investing the investors need to do their work. That means an end to end look at the company, and not just at the numbers and forecasts. Too often investors think due diligence should focus on tiny, mainly financial, details and they miss out on the obvious flaws.

My favourite example of investors missing the obvious was NZ Telecom’s sale of Yellow Pages for NZ$2.24 billion in 2007 to sophisticated private equity investors. The investors certainly looked at the numbers, but failed to look at the end users – who were already rapidly migrating away from paper pages towards online and mobile services. The result was huge losses for those investors – huge and very obvious losses for anyone that really thought about the future of phone directories.

For IP-related companies like Theranos it’s easy to talk fast and show the magic, so you want to be investors who really understand the technology, and who can actually walk the floor, talk to the scientists and technicians, look at the patents and make sure it all works as they say it does. It’s clear several rounds of investors didn’t really do their job here.

With pre-commercial IP, which we see at Return on Science, it’s expected that there is a lot of uncertainty and “I don’t know” answers about the business model, and how the IP will work in practice. That’s why around the table of the Return on Science investment committees are almost always at least some people who understand a particular technology and business being presented as well as people who understand investment, and usually both. Those committees are only recommending relatively small grants though – generally not even 1% of the the US$7m first round that Theranos took on board.

So we should look at the size of these Theranos investment rounds below and ask whether any investors knew what they were doing, or found it worthwhile commissioning independent experts who knew what they were doing to pore over the technology and industrial processes. Would you would commit these funds without a deep understanding and confidence in the technology?

(Source: Pitchbook)

Investors do take risks, but we should also seek to minimise the risks to the controllable things. For Theranos the earliest investors would expect to have a real risk of losing everything, and should have dived deeply into the IP, but were also backing the CEO and the team to execute well. The latest investors are no-doubt highly surprised that they will lose everything (it seems) and relied on the CEO and board telling the truth. It’s a shocking situation and yet they will all be asking how they could have prevented the loss.

It’s not often, I hope, that a company is built on what appears to be layers of fraudulent behaviour (that’s what the criminal investigation is about), and it’s a nightmare for investors when the layers of trust fall apart. So what can we learn?

3 Quick Learnings

So what I take from this is a reiteration of a lessons we should all know as investors. I’ve learned all of these the hard way, luckily with my own money rather than other people’s:

- Do your own work: Don’t rely on other investors or advisors when making an investment commitment.

- Look to the facts: Be extremely wary of investing in people who talk well but don’t deliver results, and actually touch the merchandise – visit the engine room of the company and make sure everything smells properly.

- Treat every round as a new investment decision: Do not assume that because you or others have invested previously that the company is a good investment.

Great article on some of the issues with early stage biotech investment, but it’s also not uncommon for the scientist to get told they don’t understand the financials or the risk:return profile of an investment, so their concerns are not that important and the risks are justified.

From a scientist’s perspective (and ex-IP lawyer turned international pharma marketing consultant), your starting point is to not believe anything until proven otherwise, which can run counter to an investor’s opinion that has already been formed. I’ve certainly called out paper-thin data being passed off as ‘the science’ behind a business after being asked to support an early stage company by an investor, only to have the air turn blue after telling the investor that the data and IP had more holes in it than a pin cushion and the investment was a lemon. Notably, the outcome was us being told by the investor, who had no technical science experience, that we didn’t know what we were talking about.

Anyone experienced in biotech or pharma knows the levels of scrutiny that routine marketing materials go through, let alone investments, but again you have to ask who these investors are and whether or not they are personally experienced in biotech to make an objective assessment of the science. Theranos certainly looks like something out of the Wizard of Oz now.

LikeLike