It is sad to see that the administrators called into Wynyard Group today. This should never happen, especially to what was a very well funded company.

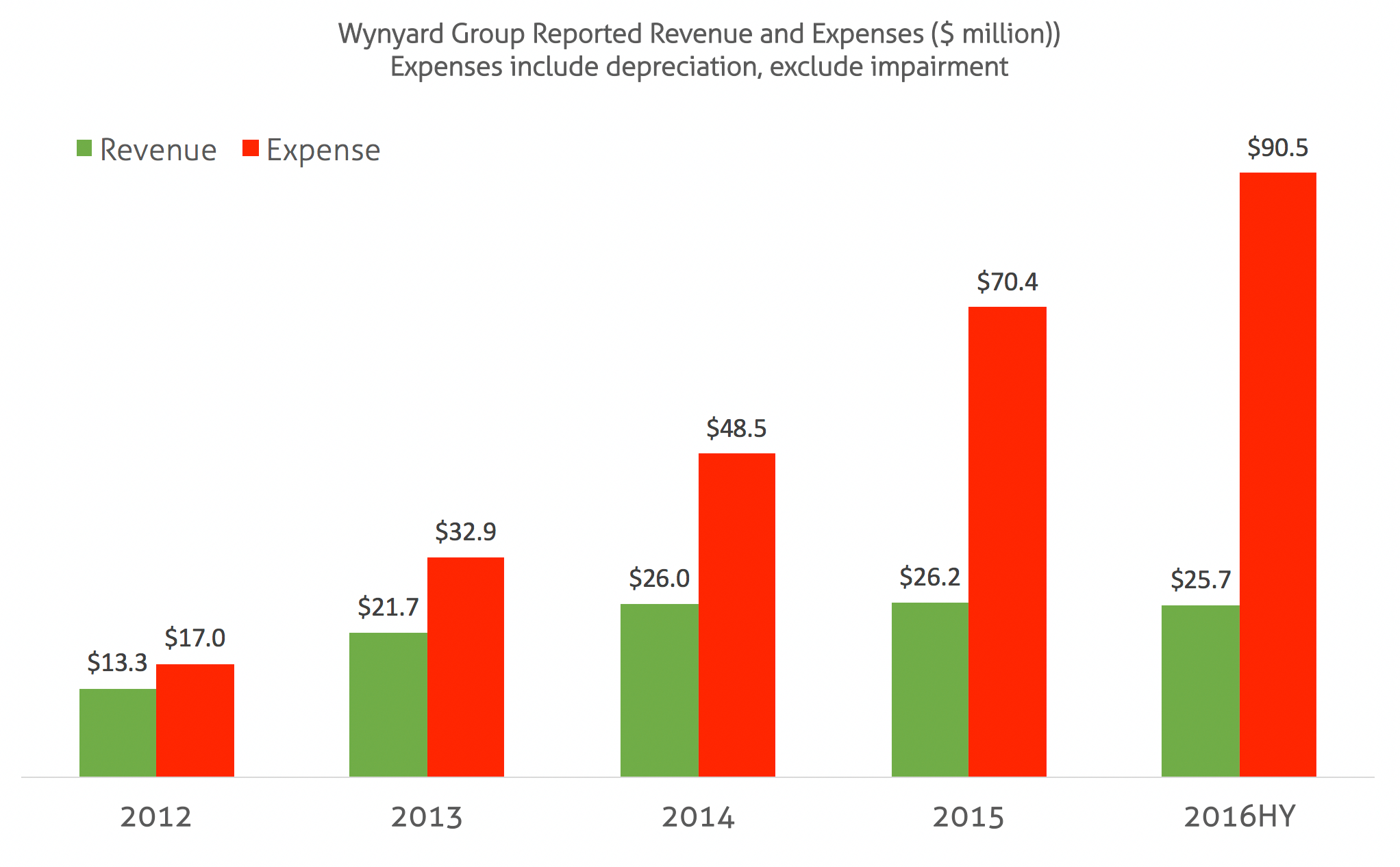

The cause is made pretty clear from the revenue and expense chart below:

(Source – Wynyard annual and interim reports. Please don’t quote this – the 2016 half year numbers are annualised, not all the years overlap as they changed their year-end date, and this includes depreciation but excludes interest and tax)

In a high growth company the norm is to raise money based on future revenue growth. If that growth does not transpire then the value of the company falls, and sharply. Wynyard’s share price fell 88% before the trading halt as a result of promised growth not appearing.

The right thing to do is pretty obvious, but hard, and that is to stop the red bars’ steady march upwards before the funding runs out. However the more palatable alternative is to keep raising money, but that gets increasingly tough when the investors do not see revenue growth, as Wynyard found out. As you keep flailing the investment terms get increasingly toxic, again as Wynyard found out.

Wynyard’s revenue guidance excludes a huge potential government contract, and that is likely in jeopardy now, as are all existing contracts, which I would expect may have out-clauses that speak to one party being placed into administration.

The tough decision that was not made

The board is to blame here – not the management team. The board failed to plan for the contingency of the growth not occurring, and the expenses should have been dramatically reduced so that the funding could last longer, or forever.

The company had $14.7 million in cash, $8.9 million in receivables and $12.8 million in payables at the end of June 2016 – net cash of $10.8 million.

But they also reported negative operational and development cash flow of $28.8 million in the 6 months to June 30, 2016, and despite raising funds then they really should have panicked.

That same interim report, dated 6 weeks ago on 12 September 2016, noted:

“it is the considered view of the directors that the Company and Group will have access to adequate resources to continue operations for at least a period of 12 months from the date of signing these interim financial statements.”

But later noted, :

“The directors are in the process of undertaking a strategic review of the Group’s operations and product portfolio. This review also includes an assessment of the plans should one of more of these material uncertainties result in an adverse impact on the forecast cash position of the Group.”

That second statement is normally code for major changes, including redundancies, in a business. But while the investor presentation released at the same time as the interim report itself showed that Wynyard had already reduced staff from 306 to 250 FTE, it is clear today that the process had not continued, at least not aggressively enough.

At over $20 million in annual revenue and $10 .8 million in cash Wynyard easily had enough funding to support 150 highly professional people, but not 250 people and their associated spend. The board needed to make the cost cutting decisions earlier, well before administrators were called in to make it for them.

Meanwhile the staff who would have been let go can be easily placed elsewhere in the vibrant New Zealand high-growth ecosystem, and it serves them and other staff poorly to let the business go to the accounting-based administrators.

I have been upset about this happening with other companies, and I consistently blame the boards of directors for this failure. It’s not an attack on the individuals, though in this case we see that there has been some recent churn, perhaps over this issue. I am sad but not surprised that this relatively new board chose the nuclear option, as it seems they had run out of time to chose the cost cutting approach, and their potential creditors were offering toxic terms.

What to do when times are tough?

I have some experience here – as currently I’m a director for 15 high growth companies, and an investor in more either directly or through Punakaiki Fund. It is very normal, in the high-growth space, for companies to go through periods where cash management is critical.

In these times the board, and that means the founders as well as the external directors, need to make tough decisions. That usually means reducing the number of staff, the costs of the founders themselves and reducing scope to make the company viable. I’ve been involved in these processes many times, and a smart board does it very early if not constantly. (It’s a lot easier to bear also when the directors are not paid – something to watch out for in very early stage companies.)

I’ve always been really pleasantly surprised at the support the company and founders are given when this is done well – staff generally understand that in high growth businesses things are uncertain and that the company needs to survive before it can thrive.

It’s always possible to survive – if a company has enough revenue, and even then a company with revenue less than one person’s salary can always be run as a supplement to that person being employed elsewhere.

The flip side of this is managing growth – a high growth company needs to change quickly to keep in control as their revenue spirals upwards. That’s a much more fun problem to solve.

As an investor I like seeing companies that have been through the fire of a financial crises, or who have started with essentially no funding. Those companies have worked out exactly what is and is not required to survive, and any funds applied are put to good use.

Wynyard’s origins as part of a larger concern perhaps meant that they have never experienced this, and so their burning moment is altogether far too public. Let’s hope that from the ashes we can see emerge a smaller but much stronger company.

I recall when the Stuff NZ had published that Gareth Morgan and his son, Sam ‘backed the Wynyard Group’ with them “both buying in”.

http://www.stuff.co.nz/business/industries/8876854/Morgans-back-Wynyard-Group

I was rather surprised and miffed at the same time (“…Medusa system was being built for “FGA” with funding from the Foundation of Research Science and Technology, the body that handed out New Zealand government research grants”.), to learn my tax money has enabled this company to aid and abet in worldwide spying by providing the likes of UK GCHQ these cyber products ), and to read this morning this article by The Intercept, PRIVATE EYES The Little-Known Company That Enables Worldwide Mass Surveillance Courtesy of Ryan Gallagher and Nicky Hager.

The Medusa system. “The technology was designed by Endace, a little-known New Zealand company. And the important customer was the British electronic eavesdropping agency, Government Communications Headquarters, or GCHQ”.

LikeLiked by 1 person

Agree wholeheartedly Lance. From what I see, the cash burn and capital management at Wynyard left a lot to be desired.

Another issue is that the nature of their sales suggests that their sales cycle has/had a very long lead time – selling to government departments and enterprise level clients by nature has a very “lumpy” revenue pattern, and one that smaller, under-capitalized tech companies can find lethal.

Wynyard may have also been trapped in a vicious circle. As news of their capital deficiencies became clear in the media, then that would have made their job selling their software that much harder. No doubt that competitors in the same space as Wynyard would have highlighted Wynyard’s issues as reasons to buy from them and not Wynyard.

LikeLike