We have kept relatively quiet at Punakaiki Fund while everyone has coped with the US election result and then the huge earthquake and aftershocks. It didn’t help that Ireland toppled the All Blacks – although that at least was well deserved.

Our offer was meant to close today Wednesday 30th November, but due to the events above we have just extended this to 20th December, 2016.

We will issuing shares soon to those who have invested already, and will be sharing news on any new investment commitments we make.

We currently have $1.44 million in applications, with $640,000 of that via Snowball Effect and the remainder directly with Punakaiki Fund.

We have investments with several companies which have offices in Wellington and Christchurch, or with staff in those areas. All staff are safe. Some families were temporarily evacuated from low-lying areas during the tsunami threat, and several were unable to access their Wellington offices for a day or two.

The good news was that almost all of the Wellington based companies had prioritised offices with high earthquake ratings, and several had recently moved for that reason. The other company was about to move offices anyway. For us this was more evidence of why we like to invest with good people with strong values.

Meanwhile most companies were able to keep working – as remote working is now a part of doing business. The Christchurch, and Wellington, earthquakes over the last few years have nudged New Zealand based companies to be very proactive on handling things after a disaster and that preparation was evident.

I’ve visited both Wellington (twice) and Christchurch since the quakes. Christchurch seems largely unaffected, while Wellington’s infrastructure has certainly suffered and there are some frayed nerves. However life goes on, and it was good to see evidence in Wellington of the staunch just-get-on-with-it attitude that has served Christchurch so well.

Our continued best wishes to everyone in Wellington, Christchurch, Kaikoura and places in between.

Revenue Growth Continues

Almost all of the investments (i.e. the underlying businesses) are unaffected – with revenues mainly from offshore or with clients able to cope. One company, NZ Artesian Water, saw sales go up sharply, as they supplied increased demand from supermarkets in the South Island and even farmers in the Kaikoura region. Others have continued to land important deals, with Melon Health in particular securing some strong clients.

Invest in Punakaiki Fund

Now that the dust has settled, the All Blacks and Black Caps are winning matches and the weather has improved it’s perhaps time to consider investing in the future of NZ – our high growth ecosystem. Please have a look at the PDS, and do consider joining the over 500 others who have already invested in this and previous rounds.

As this post mentions Punakaiki Fund Limited it could be construed as an advertisement for our public offer for New Zealand residents. So here is the link to the Product Disclosure Statement and you can invest online at Snowball Effect or directly with us.

The main reason for the post about Trump yesterday was to make the point that the US economy is strong, and, as a friend who is in Boston just messaged me, “People will get on with it” and that “they are relieved it is over.”

But I want to dive deeper into the potential impacts for New Zealand, which are not all that bad, jokes about US emigration to New Zealand aside.

The guiding presumption is that Trump will downplay some of his more radical rhetoric – especially his foreign policy statements implying he would use nuclear weapons. If that happens then all bets are off, but he is a lot smarter and will be better advised than his campaign would lead us to believe.

Trump wants to propose a constitutional amendment for term limits for congress members – but that will be very hard to get past those congress people themselves. The perverse result would anyway be more power to the funders, rather than less.

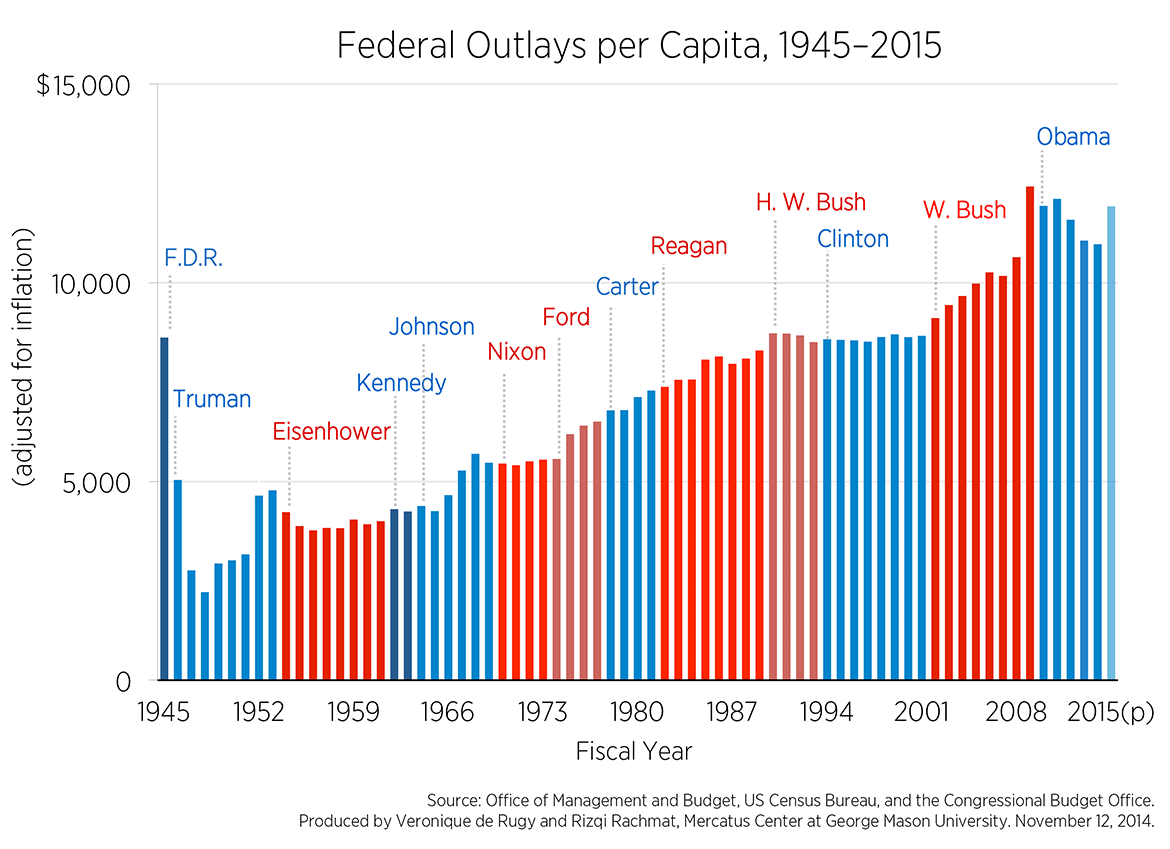

He also wants to reduce the payroll to government, which every Republican president wants to do and few to none have ever achieved, as the chart below makes clear.

Trump also wants to renegotiate or exit NAFTA, label China a currency manipulator (which will kick in trade barriers) and not sign the TPP. These are all doable – even NAFTA, which requires use a letter and six months notice to the two counter parties.

Trump will also remove environmental protections, unleash development of fossil fuel projects and cease climate change mitigation efforts.

He intends, and with a Republican Congress he is likely to, to lower the corporate tax rate to 15%, allow offshore funds to be repatriated at 10% tax and lower tax for rich people. That will be an interesting trick considering the promise to increase spend on military and a need to not overspend too much. On the other hand increasing deficits when long term interest rates are so low is not silly at all.

Obamacare is for the chop, but neither Trump nor Republicans have any credible alternative yet, so expect turmoil and plans written by health care industry lobbyists to dominate. Trump also promises to make FDA drug approvals faster, which has good and bad implications.

Finally there are a number of anti-immigration measures, including the fabled wall, deporting 2 million people, tighter immigration checks and suspending immigration from “terror-prone regions.” These have a concerning police-state overtone.

There is more, including changing the balance of power in the Supreme Court, funding for non-public schools, tax deductions for childcare and eldercare and PPP programs to invest $1 trillion in infrastructure. That last one could be interesting – the USA’s transport infrastructure, for example, is long overdue for an overhaul.

It’s not all workable – but elements will certainly get through.

Beyond the 100 day plan Trump has incited racism, sexism and a general anti-education sentiment in the USA. It’s worrying to think about where this will end, and the USA certainly has unfinished business with slavery, the civil war and indigenous Americans.

Implications for New Zealand

The main potential implications for New Zealand, I see, are changes in the US economy, changes in trade barriers and climate change mitigation progress. The other policies, while huge domestically in the US, do not really change things in New Zealand.

We do, however, have to be aware of and deal very quickly with the real issues that Trump and Brexit voters are concerned about, lest we fall in the same direction. That’s up to all of the political parties here, and National especially as the government. They are doing remarkably well for a 3rd term right of centre government, but more is required.

We are lucky to live in one of (if not the) best places in the world, and our politicians do care about social issues as well as driving business.

The US Economy

A change in the US economy would affect demand for imports, global investment returns and pricing of local investments.

The economy is due for some turmoil but overall Trump is a pro-business president. The policies he is pushing for, along with the Republican House and Senate, will defang or remove business oriented regulations, like environmental and safety mandates. Those taxes on business and high net worth individuals will fall and little to change in reality for Wall Street.

On the downside some sectors and people will suffer, in particular businesses exposed to elements of health care, the environmental sector and, more critically, people with low income who need government support. It’s a strongly held belief by many Republicans n power that cutting taxes at the expense of social payments is a good, and as Trump’s budget is ludicrous something has to give.

Meanwhile other sectors will boom, including, at least temporarily, industry exposed to fossil fuels and those infrastructure projects.

The US Equities Markets will be fine in the short to medium term. Investors are realising this, and, despite the dismay at Trump’s election, share prices are rebounding.

Indeed it would be surprising for a billionaire to do much to cripple the global investment markets – as that’s the primary way for billionaires to make money. I would not be surprised to see some market volatility as the reality of Trump’s appointees and policies become clearer over the next few months. But despite his rhetoric I don’t expect to see a sabre-toothed regulator placed over Wall Street, and expect other “business friendly” policies to emerge. I put business friendly in quotes as defanging regulators is a short term move – and tends to foster crises later on.

Meanwhile the sheer size of the US economy is hard to grasp sometimes. Their GDP is over $18.565 Trillion, and increased by $509 billion in the last year. Let that sink in – the USA grew, at $509 billion, by 2.8 times the size of New Zealand’s own GDP last year. The US GDP itself is 100 times as big as New Zealand’s GDP and the market is bottomless for New Zealand exporters.

Exporters to the USA

A change in the trade barriers would affect New Zealand’s relative ability to export and get good margins for products and (to a lessor extent) services in the USA.

Companies marketing to the US do so because of that vast economy size size. The economy growth rate is a relatively trivial factor versus the addressable market.

What’s more important is the confidence that US buyers have. New Zealand companies exporting to the US often do so on a basis of delivering something that is better and cheaper, and it’s in tough and turbulent times when buyers are looking for alternatives. So if times get tough we can rely on the size of the US market and hungry buyers looking for alternatives, and it times are good – well then times are good.

Trump wants to tear up trade agreements, and that means we can expect to see high tariffs on imports. While that’s going to affect New Zealand companies exporting to the USA, our existing trade agreements with the USA are not that great anyway. Given that we have a poorer deals than Canada, Mexico or even Australia then we will gain comparatively if they are broken and the stasis quo remains with New Zealand.

The TPP won’t pass, although we could be surprised. It was a poor trade agreement per se, and especially for us as it skewed sharply to the USA with, for example, chilling copyright provisions dictated by the MPAA and RIAA. Overall it seemed too complex to deliver the comparative advantage to each country – economic benefits that Adam Smith and David Ricardo rightly pointed 200 years or more ago.

Perhaps we now have the opportunity to recast TPP a treaty for the remaining countries, removing the US-imposed clauses before that happens, and adding maybe some more protection for domestic workers in each country. New Zealand could even take the lead on this, redrafting a simplified agreement that leaves in the benefits granted to every other country but takes out those demanded by the USA.

Net net – I see that New Zealand exporters of physical goods may be affected, and especially commodity exporters. But commodity exporters have it coming, and they should at least be well diversified, but more importantly adding more value to their products. (Fonterra – please call Lewis Road Dairy and ask about their margins.) High value products are less affected by price and tariffs, so it’s another nudge to New Zealand exporters to move up the value chain. Companies selling mainly services, such as SaaS, should not be affected, as these are too easy to deliver from anywhere without barrier.

Early signs for one hardware exporter that I know well are good – their own distributors are very positive about the future, perhaps seeing less regulation and tax as driving their businesses forward faster.

Climate Change

Trump’s climate change denialism is real – he has been consistent on this for years. Coupled with a Republican House and Senate, many of whom are who are underwritten by the Koch brothers, we can see that regression is certain.

The impact on New Zealand is the global impact – the loss of momentum to lower emissions and the acceleration of sea rise, extreme weather events and loss of habitat.

On the positive side, however, it’s increasingly clear that the switch from fossil fuels is becoming realistic without subsidies – especially if subsidies to the older industries were removed. Tesla and Wrightspeed are showing the way to a electric future that delivers better products (like faster cars), cheaper costs and reduced emissions. The price of solar generated power is falling fast, and once installed they are there forever. States, like California, meanwhile can and will keep their own incentives for lower emission approaches.

Here in New Zealand there is little we can do about the climate change policies of the USA – except for leadership by example. We do not have the funds to invest in the next Tesla, but we do have the ability to nudge, as Vector is doing, to a better future.

Impact on New Zealand based High Growth companies

The high growth New Zealand based companies that are doing business in the USA, and I am not constraining this to those with Punakaiki Fund investment, are succeeding because they are providing disruptive services. A disruptive product or service does well in a disrupted society, as buyers are looking for change. Pushpay provides alternative easy payment mechanisms, Melon Health lowers the cost to insurers paying for delivering health care, Vend makes it easy for stores to set up and expand and Xero changes the way the accounts are done, while reducing costs.

There will be category winners and losers, absolutely, with Orion Health’s share price affected today, but overall high growth companies are far more concerned about the next sale than the overall economy.

They are, like every company, potentially affected by exchange rates. But it works both ways, as if the USD falls versus the Kiwi then we will probably see other currencies rise to compensate. Companies will also see benefit in reduced costs, especially for high cost things like Amazon Web Services (AWS).

Above all this shows, as Brexit did, that it pays to diversify your markets. Punakaiki Fund’s portfolio is only abut 15% exposed to the US market, so we are not expecting any material change. And for those bashing Xero’s relatively slow uptake in the USA – the same benefit applies to them.

However so far we’ve seen little negative change in currency rates or market indicators, but I feel for the people of the USA. This post is about the effect on business here in New Zealand, but I worry deeply about the effects of the divisive campaign led by Trump.

As this post mentions Punakaiki Fund Limited it could be construed as an advertisement for our public offer for New Zealand residents. So here is the link to the Product Disclosure Statement and you can invest online at Snowball Effect or directly with us.

It’s hard to see much hope for the world now, but let’s look for some brightness in the despair of the prospect of a Trump presidency.

10: The entertainment will not stop – especially when Trump gets his Twitter account back.

9: Trump clearly doesn’t like hard work, so don’t expect him to drive through major changes in legislation that require that.

8: The Republicans in the House and Senate have huge differences of opinions with Trump – so expect some issues will never be resolved.

7: At heart Trump is really a liberal on many social issues, so if he has a conscience don’t expect too much action on LGBT rights or abortion. Sadly he doesn’t seem to have a conscience.

6: It’s going to be a lot cheaper to travel to and buy things from the USA, just like the UK at the moment.

5: The US economy is vast, irrepressible and resilient – it can and will keep steaming ahead, despite what happens in Washington. Wait for the stock markets to drop 40% then invest. Or maybe 60%.

4: Gun sales will fall, as they only rise with Democratic presidents, especially black ones.

3: Expect an abundance of news about the clueless and constantly churning staff working for and placed by Trump.

2: Fox News and their ilk will have nobody else to blame for their manufactured woes.

1: New Zealand tourism will boom – although we may have to enforce immigration law for US visitors.

Today someone in a van full of workers threw egg at me, while I was cycling to work. He was a lousy tosser, and the egg ended up on the street. It was as I was waiting to turn right into Commerce St from Quay St.

I chased the van down, much to their surprise, and the driver stonewalled and denied everything. I suspect I could have got more empathy out of the rolled up carpet in the front seat next to him – it was pretty obvious that someone in the van had thrown the egg.

I didn’t call the police – there was no time, and is it worthwhile to call 111 for assault with an egg? I didn’t even get a photo of the van, but here are the eggy remains after I returned from chasing the van.

Last week somebody stole my bicycle – it was locked up right in front of the ATEED, NZTE and Callaghan office building – and taken while I was inside NZTE’s offices assisting them help a number of high growth companies.

I got a lot of kind offers to help, including from someone inside ATEED. But there is no video track record of the bike’s last movements and the chances of recovery are slender. Do look out for those copper pedals though – they are quite distinctive.

Yesterday I was riding our tricycle down a temporary short one-lane road by Victoria park – put in place for the Auckland marathon. The driver of this NZ Bus car, which I caught up to later, wasn’t content with waiting a few seconds and honked and honked from behind me, even though there was no place safe for me to go. The trike normally carries our wee baby – this time it was just a trolley’s worth of groceries at risk.

These NZ Bus cars, by the way, are constantly illegally parked in the bus lane on Victoria Street West, opposite the park. I’ve yet to see one ticketed.

The day before this numpty driving a truck decided to do a multipoint turn in the middle of Quay St during the pedestrian phase of the lights in a weekend that saw a cruise ship in town.

None of these incidents were reported officially. Our family has tried that before. The worst incident was where a woman driving a car deliberately went through a stop sign, hitting and almost killing my wife who was on a bicycle. The driver was not charged with anything, despite a traumatic visit to the police station and provision of plenty of evidence. While the woman who was driving made a mistake, it was one that almost resulted in death and the onus was on the police to handle this with the correct emphasis. They did not.

I see plenty of other bad behaviour when I’m on my motorcycle, driving my car or walking.

Riding a motorbike has long been accepted as a risky endeavour and we all know that riders need to be constantly vigilant. We know that drivers will turn on front of us, even deliberately try to move towards us, and the recent spate of distracted phone watching drivers are a nightmare to navigate. Motorcyclists can spot lousy and distracted drivers within a second or two – and so can the police. They are not fooling anyone, including themselves.

People in cars, meanwhile, are well protected by infrastructure that favours them and strong safety systems in cars. Have a crash an you will almost certainly walk away, at least at city speeds.

But there is no protection for people walking across intersections when drivers of cars or trucks choose to run the red lights. There is increasing but still little protection for cyclists, who have far greater exposure to be hit by those cars. There is no mandate for side-protection on trucks to prevent tragedies that result in death. The distracted driving rules still allow for touching phones – whereas in NSW the far more effective rule is that you can only do so when passing it to someone else.

Accountability

What people do is driven by their values, and also to some extend by what they feel they can get away with. New Zealand has worked hard on changing the values associated with drink-driving, and backed it up with testing campaigns that are seen positively. However it’s still too easy to get away with distracted driving, red light running in Auckland (and really only Auckland) and driving dangerously near people cycling and walking.

And of course the few egg tossers are unaccountable for their actions.

I’m a big boy and able to cope with a lot, but we are talking here about potential and actual fatalities. We talking about children, babies (including ours), grandparents and commuters. We are talking about people walking to work, cycling in a new country and trying to get fit. It’s not funny to swoop near cyclists, to run red lights while tourists are crossing the street, to steal or to an egg tosser.

What can we do.

First – let’s keep installing infrastructure that separates vehicles and humans, and that encourages slower traffic. The shared spaces in Auckland are working extraordinarily well, and the physically separated bike lanes are encouraging a broad mix of people to add cycling to their mix of transport.

Secondly – let’s get serious about the magnitude of offences that are likely to cause fatalities and enforce them. Distracted driving in a downtown area feels, as a pedestrian or cyclist, a lot more dangerous than speeding, so why not elevate it to the level of dangerous driving?

Why not introduce the NSW rule about touching phones? Shouldn’t running red lights downtown with hundreds of pedestrians around be classified dangerous driving as well?

Shouldn’t we place the burden of guilt for injury of a person walking or cycling on the person driving the motor vehicle?

Thirdly – let’s use existing and new tools to change behaviour. Auckland is covered in connected cameras, and it should be relatively simply to turn on functionality that allows red light runners to be automatically caught, to review footage to follow up on egg tossers and dangerous drivers, and to provide that information to the Police.

Let’s also put in place processes where transport police are actively capturing evidence provided by members of the public over the internet – whether through a website or picked up from social media.

Finally let’s put in place processes to make sure that every incident results in an action, triaged by severity based on the level of hazard created. If this needs dedicated police then sobeit – but it will be a far more effective use of time than random driving.

We can do this. I was living in Melbourne when the introduction of speed cameras dropped the average speeds on major roads by 20-30 kph overnight. Nobody liked it, but less people died.

I am not advocating for a Police state – nor a constant citizen watch state. I am advocating for moving the needle so that we can reduce the most dangerous activities and help change behaviour before too many people die. We have a great opportunity to do this in downtown Auckland – so why not start there?

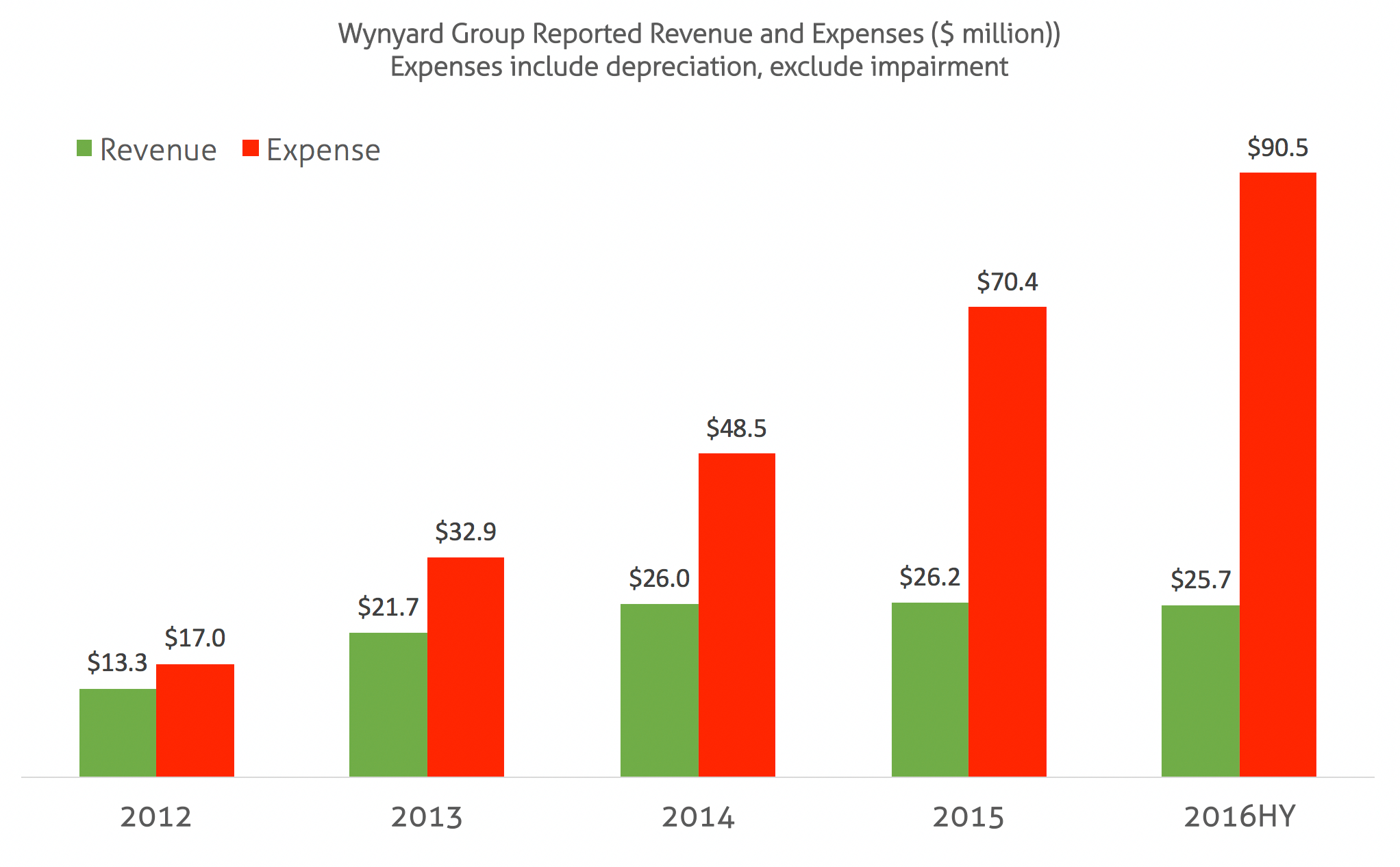

It is sad to see that the administrators called into Wynyard Group today. This should never happen, especially to what was a very well funded company.

The cause is made pretty clear from the revenue and expense chart below:

(Source – Wynyard annual and interim reports. Please don’t quote this – the 2016 half year numbers are annualised, not all the years overlap as they changed their year-end date, and this includes depreciation but excludes interest and tax)

In a high growth company the norm is to raise money based on future revenue growth. If that growth does not transpire then the value of the company falls, and sharply. Wynyard’s share price fell 88% before the trading halt as a result of promised growth not appearing.

The right thing to do is pretty obvious, but hard, and that is to stop the red bars’ steady march upwards before the funding runs out. However the more palatable alternative is to keep raising money, but that gets increasingly tough when the investors do not see revenue growth, as Wynyard found out. As you keep flailing the investment terms get increasingly toxic, again as Wynyard found out.

Wynyard’s revenue guidance excludes a huge potential government contract, and that is likely in jeopardy now, as are all existing contracts, which I would expect may have out-clauses that speak to one party being placed into administration.

The tough decision that was not made

The board is to blame here – not the management team. The board failed to plan for the contingency of the growth not occurring, and the expenses should have been dramatically reduced so that the funding could last longer, or forever.

The company had $14.7 million in cash, $8.9 million in receivables and $12.8 million in payables at the end of June 2016 – net cash of $10.8 million.

But they also reported negative operational and development cash flow of $28.8 million in the 6 months to June 30, 2016, and despite raising funds then they really should have panicked.

“it is the considered view of the directors that the Company and Group will have access to adequate resources to continue operations for at least a period of 12 months from the date of signing these interim financial statements.”

But later noted, :

“The directors are in the process of undertaking a strategic review of the Group’s operations and product portfolio. This review also includes an assessment of the plans should one of more of these material uncertainties result in an adverse impact on the forecast cash position of the Group.”

That second statement is normally code for major changes, including redundancies, in a business. But while the investor presentation released at the same time as the interim report itself showed that Wynyard had already reduced staff from 306 to 250 FTE, it is clear today that the process had not continued, at least not aggressively enough.

At over $20 million in annual revenue and $10 .8 million in cash Wynyard easily had enough funding to support 150 highly professional people, but not 250 people and their associated spend. The board needed to make the cost cutting decisions earlier, well before administrators were called in to make it for them.

Meanwhile the staff who would have been let go can be easily placed elsewhere in the vibrant New Zealand high-growth ecosystem, and it serves them and other staff poorly to let the business go to the accounting-based administrators.

I have been upset about this happening with other companies, and I consistently blame the boards of directors for this failure. It’s not an attack on the individuals, though in this case we see that there has been some recent churn, perhaps over this issue. I am sad but not surprised that this relatively new board chose the nuclear option, as it seems they had run out of time to chose the cost cutting approach, and their potential creditors were offering toxic terms.

What to do when times are tough?

I have some experience here – as currently I’m a director for 15 high growth companies, and an investor in more either directly or through Punakaiki Fund. It is very normal, in the high-growth space, for companies to go through periods where cash management is critical.

In these times the board, and that means the founders as well as the external directors, need to make tough decisions. That usually means reducing the number of staff, the costs of the founders themselves and reducing scope to make the company viable. I’ve been involved in these processes many times, and a smart board does it very early if not constantly. (It’s a lot easier to bear also when the directors are not paid – something to watch out for in very early stage companies.)

I’ve always been really pleasantly surprised at the support the company and founders are given when this is done well – staff generally understand that in high growth businesses things are uncertain and that the company needs to survive before it can thrive.

It’s always possible to survive – if a company has enough revenue, and even then a company with revenue less than one person’s salary can always be run as a supplement to that person being employed elsewhere.

The flip side of this is managing growth – a high growth company needs to change quickly to keep in control as their revenue spirals upwards. That’s a much more fun problem to solve.

As an investor I like seeing companies that have been through the fire of a financial crises, or who have started with essentially no funding. Those companies have worked out exactly what is and is not required to survive, and any funds applied are put to good use.

Wynyard’s origins as part of a larger concern perhaps meant that they have never experienced this, and so their burning moment is altogether far too public. Let’s hope that from the ashes we can see emerge a smaller but much stronger company.

Once again there was some good questioning from investors, and we had a lot of positive feedback about the event. We also had a number of people ask for live streaming – something which we will consider for next year.

In the formal part of the evening, which we kept short, we were very pleased that Mandy Simpson, currently COO of NZX, was voted onto the Board of Directors.

The official results are below.

September 2016 roadshow

To give existing and potential new investors a chance to hear more about the fund, and to ask questions in person, we were holding a series of events this week. These will cover the AGM and the likely terms for our proposed offer, which we are planning to launch in the next 2-3 weeks.

Monday 26: Taranaki – get in touch with chris@lwcm.co.nz Tuesday 27th: Wellington. 5:30pm at the Z Shed, 3 Queens Wharf Wednesday 28th: Nelson – get in touch with lance@lwcm.co.nz Thursday 29th: Christchurch – 5:30pm EPIC, 76/106 Manchester St. Friday 30th: Dunedin – 4:30 pm, top floor John Wycliffe House, 265 Princes St.

All existing and potential investors are invited, and we welcome any media as well.

2016 Annual Meeting – Official Results The following resolutions were put to the shareholders of Punakaiki Fund Limited at the Annual General Meeting held on Thursday, 22 September 2016:

1. That Ms. Amanda Simpson be appointed as a director of Punakaiki Fund with effect from the close of the AGM.

2. That Graeme Lance Turner Wiggs, who retires by rotation in accordance with clause 14.3(d) of Punakaiki Fund’s Constitution and being eligible, be appointed as a director of Punakaiki Fund with effect from the close of the AGM.

3. That Ernst Young continue in office as the auditor of Punakaiki Fund, and that the Board be authorised to fix their remuneration for the forthcoming financial year.

All of the resolutions passed, with the summary of the votes below.

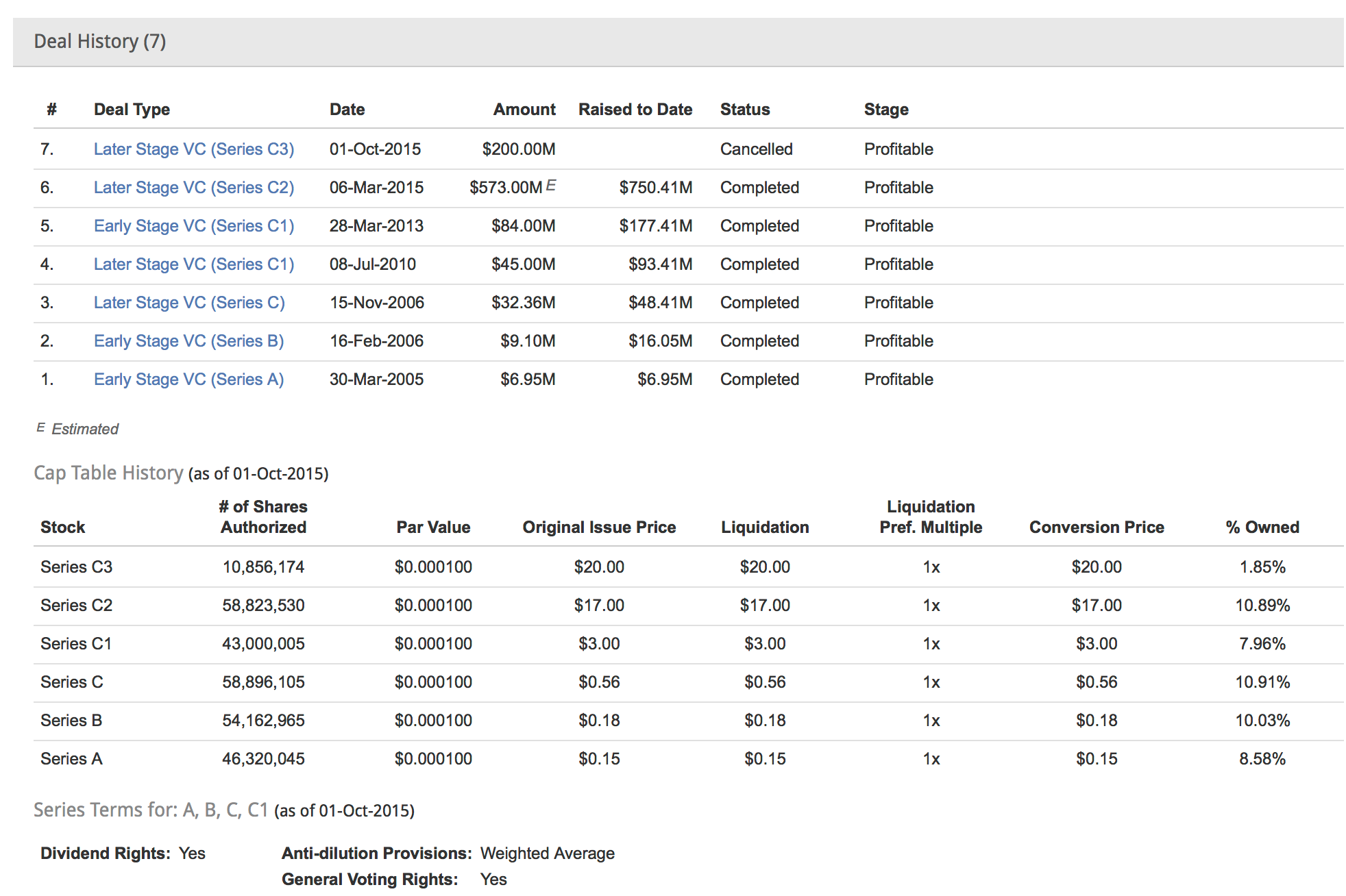

The last round of VC investors into Theranos makes for somber reading. In March 2015 Theranos raised an estimated US$573 million for their 6th round, making a total of $750 million raised. Their 7th round, for $200m, has apparently blown up before completion. Theranos was selling a blood testing service that apparently needed tiny amounts of blood to work.

The 5 investors from March 2015 should be deeply ashamed, as should those who almost committed in the 7th round.

So how do you stop this sort of dumb investment happening?

At the earliest, and every, stage in investing the investors need to do their work. That means an end to end look at the company, and not just at the numbers and forecasts. Too often investors think due diligence should focus on tiny, mainly financial, details and they miss out on the obvious flaws.

My favourite example of investors missing the obvious was NZ Telecom’s sale of Yellow Pages for NZ$2.24 billion in 2007 to sophisticated private equity investors. The investors certainly looked at the numbers, but failed to look at the end users – who were already rapidly migrating away from paper pages towards online and mobile services. The result was huge losses for those investors – huge and very obvious losses for anyone that really thought about the future of phone directories.

For IP-related companies like Theranos it’s easy to talk fast and show the magic, so you want to be investors who really understand the technology, and who can actually walk the floor, talk to the scientists and technicians, look at the patents and make sure it all works as they say it does. It’s clear several rounds of investors didn’t really do their job here.

With pre-commercial IP, which we see at Return on Science, it’s expected that there is a lot of uncertainty and “I don’t know” answers about the business model, and how the IP will work in practice. That’s why around the table of the Return on Science investment committees are almost always at least some people who understand a particular technology and business being presented as well as people who understand investment, and usually both. Those committees are only recommending relatively small grants though – generally not even 1% of the the US$7m first round that Theranos took on board.

So we should look at the size of these Theranos investment rounds below and ask whether any investors knew what they were doing, or found it worthwhile commissioning independent experts who knew what they were doing to pore over the technology and industrial processes. Would you would commit these funds without a deep understanding and confidence in the technology?

(Source: Pitchbook)

Investors do take risks, but we should also seek to minimise the risks to the controllable things. For Theranos the earliest investors would expect to have a real risk of losing everything, and should have dived deeply into the IP, but were also backing the CEO and the team to execute well. The latest investors are no-doubt highly surprised that they will lose everything (it seems) and relied on the CEO and board telling the truth. It’s a shocking situation and yet they will all be asking how they could have prevented the loss.

It’s not often, I hope, that a company is built on what appears to be layers of fraudulent behaviour (that’s what the criminal investigation is about), and it’s a nightmare for investors when the layers of trust fall apart. So what can we learn?

3 Quick Learnings

So what I take from this is a reiteration of a lessons we should all know as investors. I’ve learned all of these the hard way, luckily with my own money rather than other people’s:

Do your own work: Don’t rely on other investors or advisors when making an investment commitment.

Look to the facts: Be extremely wary of investing in people who talk well but don’t deliver results, and actually touch the merchandise – visit the engine room of the company and make sure everything smells properly.

Treat every round as a new investment decision: Do not assume that because you or others have invested previously that the company is a good investment.

We can easily forget that most people don’t read Transport Blog, find The High Cost of Free Parking obvious or understand that great cities are great to walk in – and lousy to drive in. Many of us have lived overseas though, and we just tend to forget just how things worked over there and what is missing here.

So here are 20 (not so) obvious things about cities, and Auckland in particular, that we should all remember.

1: Many people living in a small area makes for a better life for all. It’s more efficient, more fun and increases business, and that’s why people choose to live in big dense cities.

2: Large roads create moats that block parts of cities from each other and we risk losing the benefits of urbanism. Many of the motorways that carved up cities overseas are now being removed, and the same applies to ports.

3: Parking spaces not only take up valuable land, but they also reduce the positive effects of urbanism. They are expensive and should be removed or charged for accordingly.

4: All the great cities of the world are horrible places to find and pay for a car park. That’s a design feature, as they prioritize walking and public transport to cope with the demand for moving people.

5: Public transport takes cars off the road and increases, dramatically, the ability of a city to deliver people to and from work and shops, and with very limited use of land. It is far cheaper, based on both marginal and capital costs, to move people with public transport than cars.

6: An empty rail line or bus lane is a good thing – the point is to make their lanes congestion-free so that riders can get to their destination faster.

7: Removing cars and car parks, broadening footpaths and installing shared spaces increases business (significantly) to the local merchants, and makes for higher value commercial buildings as well. People want to be in spaces that are friendly to people.

8: Apartments can be awesome places to live – and they should come in all shapes and sizes to cater for all stages of life. They are also intrinsically cheaper to build, supply with services and, with urban density, commute and shop from. You can generally survive without a car.

9: Driving to work is a horrible experience versus walking, riding and public transport – in that order. If you have the other options then take them.

10: To get people out of cars and onto cycleways and walking we need to provide pleasant and safe environments for walkers and cyclists. It’s not enough to do big projects – we need a network from homes to school, shops and work.

11: Driving kids to school is a confidence trick – switching back to kids walking and cycling will make everybody safer by removing cars from the streets, making kids healthier and providing critical mass of kids to react to and prevent any low probability but newsworthy predators. But we need to switch entire schools at a time to make this work. We also need to be smarter about buses for schools.

12: We make personal choices for transport that are not our own best interests, such as choosing to drive (and be traffic) rather than, say, walk. The right economics, such as variable tolls and parking charges and cross-subsidization of public transport nudge us into making better choices and save money for everyone.

13: New Zealand has one of the world’s most efficient domestic airline systems. Getting from the airport to Auckand city though is embarrassingly poor – great cities offer rail or light rail.

14: Autonomous cars are still cars, and risk clogging the roads even more as they reverse commute after dropping passengers. Autonomous taxis are still taxis. Neither takes cars off the roads – people will still want their Toyotas, Fords, BMWs and Mercedes Benzes with their stuff inside, while those shared cars will need constant cleaning.

15: Auckland has the potential to be one of the world’s great cities. We are rapidly building in population, especially downtown, and we need to invest to grow. That means increasing our debt funding, making sure the rates are set at the right level (they are amongst the lowest in NZ), building smart infrastructure to allow for density, removing trucks and cars by providing better alternatives and unleashing bigger buildings in and around downtown.

16: Allowing bigger buildings in your property zone will increase the value of your property – a lot. That’s free money. You may even find a developer who will buy your place for a lot of cash and give you a free apartment in their new development.

17: In large cities the houses with backyards, as we have in the leafy inner city suburbs, belong to a few extremely wealthy families. In Auckland the pressure is building to convert those houses to much higher value apartments.

18: Global warming will make beach front property more marginal – but property overlooking the coast will always be valuable.

19: Induced demand, where if you build it they will come, applies not just for roads, where new roads rapidly get clogged, but also for rail, light rail and bike lanes. The latter also increase the value of surrounding property. Build the bike lanes and they get used, and the evidence is clear to see.

20: In short Auckland needs to maintain or increase rates as a percentage of home value, borrow more, unleash the ability to build bigger commercial and residential buildings, invest heavily in public transport including rail, light rail and bus lanes, expand the walkable areas and cycle lanes, look to move the port within 10 years, say, increase the cost and reduce the supply of parking and work with schools and businesses to acelerate the transition to walking, cycling and public transport. And they can use an abundance of evidence from Auckland and offshore to make these decisions.

The reason Auckland is doing so well is that the current CEO and people that work for Auckland Council and aligned organizations as well as the private sector are working hard to achieve these goals. The central government is also largely aligned. The results, like the crowds in Britomart and Wynyard Quarter, the number of cranes downtown, the rapid rise in public transport, walking and cycling and increase in collective prosperity and delight in the inner city are clear for all to see.

However we need a Mayor and Council that support growth, that support investment and that support rather than constantly undermines the largely excellent work done by Auckland Council. We need Councillors who not only read their papers (and many don’t I’m told), but who also read and understand the vast body of work and international experience on urban and transport planning. We need Councillors who use, as National MP Simon O’Connor recently said to Parliament, reason, evidence and experts inform and make decisions. We need a Mayor and Councillors who are positive about the future of Auckland, who are inspiring and who have the skills and experience to do the work.

We don’t need Councilors who are sports or media celebrities with no real qualifications for the role. We don’t need Councillors who sayno to every proposal without reading or turning up to resident events. We don’t need Councillors who undermine the CEO and Auckland Council, such as those who voted against he Unitary Plan submission.

It’s time to professionalise Auckland Council. Let’s make sure that there are enough high quality independent and party aligned candidates for all electorates. And if you are considering standing on the sort of platform outlined above – then please do so. I’m willing to help.

For a society that provides a full range of services aren’t we remarkably low-taxed in New Zealand? I was comparing notes with my Australian-based brother this week, and the differences are stark.

Our top income tax rate is 33%, and we have no capital gains tax, while property rates (for me in Auckland) are just 0.29% of assessed value. We also have GST of 15%.

In Australia they pay 49% top tax rate (45% + 2% +2%). They also pay tax on any capital gains – the net capital gains are simply added to the taxable income, but net capital losses can’t be deducted from income. The family home is exempt from capital gains, but ordinary investments are not. You can get some relief by placing your money into a super fund – and you can self-manage this – but money going in is still taxed at 15% and is limited. If you contribute too much then the excess is taxed at 47%, and if your total income is over $300,000 in a year then there is another 15%. GST in Australia is also more complex than here, though lower at 10%.

Whew – as you can see it’s also a much more complicated system – you’ll probably need a lot more expensive advice than here in NZ.

In the USA the top tax rates are over 40% just for the federal component, then you add state tax, not to mention health insurance and all the other things that their state does not provide. It gets over 50%. Sure their system is so rigged and wretched so that the effective rate for the wealthy is lower – so be prepared to pay a lot to a CPA as well. Let’s not get started on the absurdities of cascading regional taxes, nor regional taxes on goods and services. It’s all incredibly expensive, complicated, and biased towards the very very wealthy.

I like it here – our tax system is understandable and efficient. Sure we can do better, but it’s worth pausing now and then to say “well done” to a series of governments.

We’ve seen plenty of headlines recently about offshore companies bottling our water and making fortunes. So when I met Nelson-based Kiwis Andrew Strang and Wayne Herring through a Better by Capital engagement, I was eager to see how their New Zealand Artesian Water business (NZAW) was progressing. The answer was “very well”, and that they were actively looking for funds to grow.

We are very impressed by their supply strategy – working closely with the Tasman District Council – their product and their plant, as well as their plans for expansion. Their premium alkaline water, E’Stel, comes in elegantly designed bottles and also in boxes, and is mainly sold into China, although NZAW has supply contracts across the world. They have also developed a new blended-water product for China aimed at mothers using infant formula. For now their primary challenge appears to be scaling the business to deliver on sales demand. Investors living in or visiting the South Island can help with that demand – E’Stel is available at selected retailers there.

The brothers-in-law have a background in West Coast mining, and Andrew also has a background in the high end fashion and jewellery business and a lot of experience in Asia. Their unusual combination of experiences, combining New Zealand’s natural resources with fashion sense, trading in Asia and grit started to pay off from when the Prime Minister opened their plant in March 2015, and since then the company has grown quickly.

Andrew and Wayne know how to get things done, and their story will continue to attract attention as their business grows. We are delighted to be able to join them on their journey.

The investment

Punakaiki Fund has invested in a 11.8% shareholding in NZAW, and has options to bring the shareholding up to 20%. I’ll be joining the board of directors (as I will also do for Linewize).

But is this hi-tech?

We set up Punakaiki Fund to invest in all sorts of high-growth companies, but in particular those in technology, internet and that are design-led. We increasingly believe that quality high-growth companies combine most or all of these elements, and NZAW certainly uses design and technology to gain an advantage. Their bottles, for example are square-based and round topped, but with a curve and thickness that means they not only look good on the shelves, but they also stack higher in shipping containers and are reusable. Their infant water is a designed product – building on MIT research to deliver the optimum product for babies. Most of all though we see that their growth prospects are very strong, and that our funds will help them a lot on their journey.

Managing Internet access is hard – do you allow staff or your family to view the unfiltered internet, or block everything except for approved sites? It’s even harder at schools. On the one hand, you don’t want students accessing inappropriate content, or spending their time and the school’s bandwidth frivolously. On the other hand, you don’t want to restrict their learning opportunities, for example by blocking information on breast cancer. You also want to teach students how to think critically about their own activity so that when they leave the protective environment of the school they’ll have the skills to keep themselves out of harm’s way.

That’s where our latest investment, Linewize, comes in. Their internet firewall, management and control service is easy to use, administrated centrally and gives teachers discretion about what is or isn’t allowed. It runs on just about any hardware, integrates with Google Apps For Education, is really cost effective, and most importantly, help students learn from their choices.

Linewize have sold their open source firewall and cloud-managed service solution to over 200 New Zealand schools so far, and they have done so when their main competition, Network for Learning (N4L) provides a free alternative. Linewize are winning because their solution is easy to install and manage, and it gives teachers the control they need in the classroom. They are also pushing offshore and have good early traction, and our investment will allow them to accelerate these efforts.

Linewize prices start at $75 per month for tiny schools and increase with the number of students, with a lower price per student as the roll-size grows. The product is mainly sold through a 20-strong growing network of resellers, who also install and provide the first latter of support for the product and service.

Scott and Michael

Linewize was founded by Michael Lawson, CTO, and Scott Noakes, the CEO. I’d heard about the company originally through judging the Hi-Tech Awards in early 2014, and again for this year’s awards, where they were a finalist in they category. Scott and I talked at the Hi-Tech Awards gala evening and after a series of meetings and exchanges we came to an agreement on the 31st of May. Since then we’ve worked through the legal process we all eventually signed a week ago.

Our investment will primarily help to accelerate sales, particularly into international markets and looking to double their New Zealand market share.

The Investment

Punakaiki Fund made identical investments into the two Linewize companies – Linewize Limited and Linewize Services Limited. The fund now owns 8.05% of each company and has agreed to invest another tranche, subject to fund raising, to bring the ownership up to 20%.

One of our core motivations at Punakaiki Fund is being able to help and watch companies create a large number of sustainable new jobs. And one of the best people around at hiring new people is Kirsti Grant, who was in charge of the rapid ramp-up of Vend’s team, and who is a fellow director on the board of Weirdly.

So when Kirsti and her partner Lance Hodges told us they were developing a new product that would make it easier for companies to manage hiring, we knew this was a real problem that she had felt. She and Lance backed up that experience with over 100 interviews and tests with prospective clients, and only started coding when they were sure their product had both end users who were demanding it now, and paying customers who would be willing to buy.

The company is called Populate, and while it is pre-launch, we decided that Kirsti and Lance deserved our early support.

The investment

We made a relatively small investment into Populate and own 9% of the company. The product will help companies collaboratively plan and track their hiring plans – a task done these days mainly on spreadsheets and email, or with very large and cumbersome ERP systems. Each manager will be able to track their team, plan for growth and run basic statistics on team composition. The information scales up to the company level, allowing heads of HR and CFOs the ability to forecast and manage. Populate is especially useful for companies that are growing very quickly, often much faster than an annual planning cycle can handle, and it will allow rapid and informed decisions about hiring.

We are looking forward to tracking Populate’s progress, especially their recurring revenue growth, and are delighted to welcome Kirsti and Lance to the fold.

At Punakaiki Fund we like to keep things simple, and we encourage other investors and all founders to do the same.

However in past years the contracts used for many NZ-VIF/SCIF deals have been arguably quite toxic against founders, and these can make it very hard for investors, founders and the next round investors.

But things are getting better, and it’s good to see the NZ-VIF/SCIF standard documents posted on their website.

We have also observed that these contracts are negotiable to much simpler form, and encourage founders and investors to do so.

Help is available from Simmonds Stewart, who have represented companies we have invested into. They have marked up several SCIF documents, including the latest SCIF term sheet, which I highly recommend founders and investors in this space consult.

However Punakaiki Fund goes further, and we believe the rest of the industry should to.

We would like to see contracts that are more founder-centric and less investor-centric;

We would like to see contracts that trust the boards and founders and not be prescriptive about what the business does and retain actions;

We would like to see contracts that say less, and rely on the excellent NZ law to provide investor protection;

We would like to see simpler, shorter documents that are easier to understand (and sign). (We would like to see lawyers paid less and do more deals.);

We would like to see terms where companies receive a net sum from investors and do not have to pay any kick-backs (6% in the SCIF world), investor legal fees or for any investor-directors; and

We would like to see more deals done – and simpler contracts will help that happen.

So I have taken the blue pen to the Simmonds Stewart mark-up, and here is a SCIF Term Sheet mark-up from the perspective of LWCM and Punakaiki Fund. Tell us what you think.

New Zealand’s traditional leadership in agriculture is due to our land, climate, hard work and invention from generations of farmers, and our universities and business that have supported them with increasingly valuable technology.

But our position is under threat, not today, but in the medium term certainly. The threat is that high quality food will be grown essentially anywhere for lower cost of inputs, and that global demand for meat will fall. Perhaps something’ll come along to make it easy replace milk as well.

High Density Gardening

There is a trend towards growing plants in more controlled environments in agriculture (CEA). The neat trick with high density gardening is that the control of temperature, energy and climate not only reduces the amount of inputs (water, energy and so on) but also allows for control of insects and pathogens. And when you control the access of pathogens then you don’t need so much fungicides and pesticides, if at all. The result is not only faster growing plants, but food that is almost organic in its lack of pesticides and other additives. It can be delicious.

At the moment it is relatively rare to see crops grown using tightly controlled environments for the whole lifecycle. But observe in the supermarket that some crops, such as tomatoes and blueberries, are now available – and incredibly tasty – year round. I suspect the same is happening with many high value flowers. These crops are grown in glasshouses, but there is, apparently, still a good gap between current practices and true CEA.

The goal, still fairly seldom seen, is vertical farming, with leaders like Plantagon and AeroFarms. With this very high intensity farming there is no reason why the farms need to use a lot of land footprint – a farm can be on floors of a tall building, with controlled LED lighting delivering the light-based to the plants.

But there is a problem, as it costs money to power those LED lamps, while on traditional farms the plants receive free energy from the sun.

The answer is tied up in the lowering costs of renewable energy, such solar panels, and batteries. These costs are already at to the point where it makes little sense to build traditional power plants, with Warren Buffet bragging in his latest letter that

“Berkshire Hathaway Energy (“BHE”) … … has invested $16 billion in renewables and now owns 7% of the country’s wind generation and 6% of its solar generation. Indeed, the 4,423 megawatts of wind generation owned and operated by our regulated utilities is six times the generation of the runner-up utility.

We’re not done. Last year, BHE made major commitments to the future development of renewables in support of the Paris Climate Change Conference. Our fulfilling those promises will make great sense, both for the environment and for Berkshire’s economics.”

If you are not content with a quote from a capitalist, then Al Gore has popped up with a new TED talk, The Case for Optimism on climate Change, last week and included this slide:

He also showed slides showing the precipitous fall in prices for storage batteries and solar panels. These curves will keep going, so while today it’s hard to economically justify building a thermal power plant, at some stage soon it will not be economical to even fuel a thermal power plant. Once we reach and pass that point it’s clear that generating and storing the power to drive those LEDs will be relatively cheap and a relatively low capital or opex cost for a vertical farm.

So Malthus can wait a while longer it seems. But the problem is not solved yet, as this Guardian article shows the energy requirements for indoor crops are very large.

Better Meat

But we also eat meat, and as the more of the world enters the middle class the demand for grass and grain eating inefficient methane belching animals will continue to grow. We can gain more efficiencies and control effluent and CO2 by keeping animals inside, and that’s done in many countries. If that’s the future for meat and milk then New Zealand has no structural advantage over any other country, and the resulting products will be priced accordingly at very low or negative margin.

There are alternatives – The Economist has a video article, The Meat Makers, on two companies with different approaches to replacing meat. One which is attempting to grow meat in-vitro and the other is trying to use plants to create a beef substitute. The video shows poor progress for both companies, but it does show that a lot of investment is going into moving directly from plants into meat. In New Zealand SunFed Meats is attempting the same, and seems to be making great progress turning peas into chicken.

Now if we combine the two trends together it seems logical that someone will figure out how to grow a plant that is able to be easily process into substance that we find very close to meat. Will it be tasty? I suspect that for many years a very good steak will continue to attract demand, but would not be surprised to see meat eating consigned to the same shameful dustbin as cigarettes within the next 50 years.

Malthus is wrong again

When I was younger, many years ago, I remember reading Green literature about the end of days. The World was going to run out of resources and food, and quoted Thomas Malthus, who wrote in 1798:

That the increase of population is necessarily limited by the means of subsistence,

That population does invariably increase when the means of subsistence increase, and,

That the superior power of population is repressed, and the actual population kept equal to the means of subsistence, by misery and vice.

Malthus was right, but he also thought that population would increase exponentially and food production linearly. However productivity of food (and other) production improved exponentially over the ensuing years and the techniques above will continue that trend. It’s a future where we can produce more with less, as a globe, and one where there is no need for our plants at least to not be tasty and fresh.

Existential crisis

All these trends are great for the world, but will they also trigger an existential crisis for New Zealand? If anybody anywhere in the world can use small amounts of energy, water and nutrients to create the same quality food as we can here then why would anyone buy from New Zealand? If good-enough meat made from plants is able to substitute for a large amount of meat eaten globally then won’t the demand and price for our cattle and sheep fall? And surely someone will figure out how to more efficiently produce milk from plants?

The future of New Zealand is unknown, and these trends could be decades away. But we should be leading and not reacting late to these trends. We do have a good Agri-Tech sector, with many companies helping traditional farming get more efficient, and others like Sunfed Foods and Autogrow, who make controllers for glasshouses, aiming ahead of the curve. We should support them.

We should also focus on the quality end of food production, aiming to be the purveyor of the best food in the world rather than shifting tonnes of powder and meat. We’ve moved a long way in this direction over the years, but our polluted rivers are evidence that we can no longer collectively hold our heads high.

Or perhaps there is another path – fast adoption of these intensive techniques to increase production and lower land and other resource use per output, followed by the return of some of the less productive land under grazing to native forest and birds. That’s a New Zealand we could all live in.